This article explores the market forces reshaping veterinary pharmaceuticals, from the $40+ billion global valuation to the critical role of vaccine adjuvants like QS-21 in disease prevention. We'll examine how regulatory landscapes in the U.S., EU, and China are evolving, why verified supply chains matter more than ever, and what the expansion into livestock, poultry, and companion animal sectors means for pharmaceutical buyers navigating this dynamic industry.

TLDR:

- Global veterinary pharmaceutical market approaches $40B by 2031, driven by pet ownership growth and livestock health demands

- Vaccine adjuvants enable dose-sparing and cross-protection, critical for large-scale animal vaccination programs

- Regulatory frameworks (FDA CVM, EU 2019/6, China NMPA) require specialized compliance expertise

- Supply chain integrity—cold chain logistics, verified sourcing, customs expertise—separates reliable distributors from commodity suppliers

- VuRoyal Pharmaceutical serves as FDA-registered exclusive U.S.-China distributor of veterinary vaccine adjuvants including QS-21, Vet-Sap, and Ultra

The Veterinary Pharmaceutical Market at a Glance

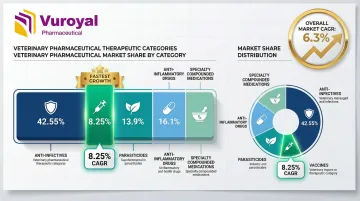

The global veterinary pharmaceutical market is experiencing consistent growth across all major product categories and geographic regions. MarketsandMarkets projects the market to grow from $27.41 billion in 2025 to $39.37 billion by 2031, representing a 6.3% compound annual growth rate. Mordor Intelligence estimates slightly higher figures, forecasting growth from $32.50 billion to $48.31 billion over the same period.

Five major therapeutic classes define the market: anti-infectives, parasiticides, vaccines, anti-inflammatory drugs, and specialty compounded medications. Anti-infectives captured 42.55% of market share in 2025, but vaccines are expanding faster at 8.25% CAGR through 2031. This shift reflects the industry's pivot toward preventive care rather than reactive treatment.

Public company disclosures confirm this trend. Zoetis reported its 2024 revenue mix as 24% parasiticides, 20% vaccines, 18% dermatology, and 12% anti-infectives—demonstrating how biologics and preventive therapies are gaining share at the expense of traditional antibiotics.

Geographically, North America commands 38.4% of the global market, with the United States alone accounting for 55% of Zoetis's 2024 revenue. Europe holds the second-largest share, while Asia-Pacific is the fastest-growing region. China's recovery of its pig herd to 440 million head in 2024 reignited demand for vaccines and prescription antibiotics — a clear example of how livestock production cycles drive regional pharmaceutical consumption.

Distribution channels are shifting alongside these trends. Traditional veterinary clinics remain primary points for routine care, but large-scale commercial farming operations are moving toward direct procurement to manage herd health at scale. This B2B shift favors distributors that can offer:

- Regulatory expertise across multiple jurisdictions

- Cold chain logistics for temperature-sensitive biologics

- Established global sourcing networks with verified supply chains

What's Driving Veterinary Pharmaceutical Industry Growth

The One Health Framework Elevates Investment

The "One Health" concept—recognizing the interdependence of human, animal, and environmental health—has transformed veterinary medicine from a secondary concern to a strategic priority. The Quadripartite One Health Joint Plan of Action (2022-2026) explicitly calls for increased political commitment and investment in endemic zoonotic disease control.

In the U.S., the CDC's National One Health Framework (2025-2029) establishes objectives to advance veterinary product research, development, and supply chain infrastructure for new vaccines and therapeutics.

This policy shift channels government funding from reactive culling toward proactive vaccination programs, creating sustained demand for veterinary pharmaceuticals.

Pet Ownership Boom Creates Permanent Demand Baseline

Post-pandemic pet ownership has permanently elevated baseline pharmaceutical demand:

- United States: 94 million households owned at least one pet in 2024, up from 82 million in 2023, driving $152 billion in total pet industry expenditures

- Europe: 139 million households (49%) own pets, totaling 299 million animals across the continent

- China: Urban pet population reached 124.11 million in 2024, with cat ownership growing 2.5% and dog ownership 1.6%

The humanization of companion animals—treating pets as family members deserving premium care—drives demand for advanced diagnostics, chronic disease management, and specialty treatments previously reserved for human medicine.

Food Security Pressures and Livestock Investment

Population growth and rising protein consumption are driving record-level investment in livestock health. According to the OECD-FAO Agricultural Outlook 2025-2034, global meat output is projected to climb 12% between 2024 and 2034. Livestock contributes 40% of global agricultural output value, making veterinary disease surveillance and pharmaceutical intervention essential to food safety and economic stability.

Commercial producers recognize that pharmaceutical solutions reducing morbidity and protecting herd productivity deliver measurable ROI through improved feed conversion, reduced mortality, and faster time-to-market.

Zoonotic Disease Outbreaks Lift Vaccine Demand

Sustained disease outbreaks are lifting demand for rapid-response vaccines. The spread of high pathogenicity avian influenza (HPAI) A(H5N1) clade 2.3.4.4b viruses led to unprecedented poultry deaths and recently spread to U.S. livestock. In response, the FDA granted conditional clearance for an H5N1 vaccine in 2025, allowing producers to vaccinate rather than depopulate flocks.

Similarly, persistent African Swine Fever (ASF) outbreaks are accelerating novel subunit vaccine development. The USDA invested $98 million in emergency H5N1 vaccine procurement after traditional alum-based formulations failed to curb viral shedding. Disease pressure, in other words, creates the commercial case for more effective adjuvanted vaccines.

R&D Investment Reaches Record Levels

Major veterinary pharmaceutical companies deployed record capital into R&D in 2024:

- Zoetis: $686 million R&D expense supporting monoclonal antibody development across five species

- Elanco: $344 million focused on late-stage blockbusters including a $130 million biologics facility expansion

- Boehringer Ingelheim: €6.2 billion total R&D with significant veterinary allocation for swine and bluetongue vaccines

This investment concentration in companion animal biologics and critical livestock vaccines reflects where manufacturers see the highest margin opportunities and fastest growth potential.

Sector Spotlight: Livestock, Poultry, and Companion Animals

Companion Animals: The Premium Growth Engine

Companion animals represent the largest and fastest-growing segment. Zoetis reported dogs and cats accounted for 65% of its $9.25 billion 2024 revenue. Grand View Research estimated the global companion animals segment generated $17.74 billion in 2024.

Growth is fueled by species-specific, customized therapies. The industry has successfully commercialized monoclonal antibodies (mAbs) and long-acting injectables that improve compliance and minimize dosing frequency. Notable FDA approvals include:

- Librela (bedinvetmab): Approved 2023 for canine osteoarthritis

- Solensia (frunevetmab): Approved 2022 for feline osteoarthritis

- Cytopoint (lokivetmab): Licensed 2016 for canine atopic dermatitis

These biologics command premium pricing and generate recurring revenue through regular dosing schedules, making them attractive pipeline investments. The same innovation pressure driving companion animal biologics extends into livestock — where disease burden, not premiumization, is the primary growth catalyst.

Swine: Disease Pressure Drives Pharmaceutical Demand

The global swine healthcare market reached $3.18 billion in 2024, projected to hit $5.59 billion by 2033 at 6.15% CAGR. African Swine Fever (ASF) and Porcine Reproductive and Respiratory Syndrome (PRRS) are the primary demand drivers.

China's unmet need for an approved ASF vaccine created conditions where counterfeit products filled the gap — until government enforcement crackdowns accelerated legitimate R&D. The result: accelerated investment in live attenuated and subunit vaccine platforms, and heightened demand for verified, compliant supply chains across the region.

Poultry: Vaccines Dominate Flock Health Management

Mordor Intelligence valued the poultry health market at $17.38 billion in 2025, projecting growth to $28.44 billion by 2031 at 8.56% CAGR. Vaccines held 47.12% market share in 2025, underscoring their role as the default tool in commercial flock management.

Water-soluble medications represent an evolving segment. Medically important water-soluble antibiotic use in U.S. broiler chickens decreased substantially from 2013 to 2017, but increased slightly from 2017 to 2023 due to rising disease incidence, such as avian metapneumovirus.

Across both poultry and swine, producers are pushing for multi-valent formulations that reduce injection frequency and animal stress. Merck Animal Health's Circumvent CML three-in-one swine vaccine reflects this cross-species trend — a practical priority when managing operations at tens of thousands of animals.

The Role of Vaccine Adjuvants in Veterinary Medicine

Technical Definition and Mechanism

The World Health Organization defines a vaccine adjuvant as an agent added to or used with a vaccine antigen to augment, potentiate, and possibly target the specific immune response. Adjuvants divide into two groups: delivery systems (mineral salts, emulsions, liposomes) that present antigens to the immune system, and immunostimulators (TLR ligands, saponins) that directly activate immune cells.

Quality adjuvant selection determines vaccine efficacy, duration of protection, and dose requirements—critical factors in both development costs and field performance. Saponin-based systems have emerged as the most studied class within that spectrum.

Saponin-Based Adjuvants: QS-21, Quil-A, Matrix-M

Saponin-based adjuvants, derived from Quillaja saponaria bark, are among the most clinically studied immunostimulators in veterinary medicine. The Matrix-M™ adjuvant demonstrates critical capabilities:

- Quil-A: Natural extract composed of multiple saponins, widely used in veterinary applications

- QS-21: Purified fraction promoting antigen-specific antibody responses and cytotoxic CD8+ T cells

- Matrix-M/ISCOMs: Formulates saponins with cholesterol and phospholipids into 40-nm nanoparticles, quenching hemolytic toxicity while targeting delivery to phagocytic cells

Clinical Benefits in Animal Populations

Saponin adjuvants provide three advantages that directly affect formulation decisions and field outcomes:

- Dose-sparing capacity: Matrix-M reduces the antigen quantity required per dose—a critical advantage during pandemic or epizootic shortages when antigen supply is constrained.

- Cross-protective responses: Matrix-M-adjuvanted vaccines recognize broader conserved epitopes, inducing cross-reactive immunity against drifted viral strains. This is particularly relevant for rapidly mutating pathogens like avian influenza.

- Long-lasting immunity: ISCOMs stimulate durable humoral and cellular responses, including CD4+ helper T cells and CD8+ cytotoxic T cells. Quil-A has induced neutralizing antibodies in cattle against foot-and-mouth disease, confirming field-level efficacy.

Adjuvant Market and Supply Chain Considerations

Mordor Intelligence valued the veterinary vaccine adjuvants market at $475.52 million in 2025, projecting $792.08 million by 2031 (8.88% CAGR). Alum and calcium salts command the largest volume share, but nanoparticle and saponin systems capture premium tiers.

Access to regulatory-compliant adjuvant ingredients through verified global supply chains remains a key bottleneck for vaccine developers. VuRoyal Pharmaceutical, an FDA-registered distributor and exclusive U.S.-China partner of Desert King International, addresses this gap by supplying GMP-certified saponin adjuvants—including QS-21, Vet-Sap, and Ultra—with full regulatory documentation and cold chain logistics support.

Navigating the Regulatory Landscape in Veterinary Pharmaceuticals

U.S. Framework: FDA CVM and ADUFA

The FDA Center for Veterinary Medicine (CVM) regulates animal health pharmaceuticals in the United States. The Animal Drug User Fee Act (ADUFA), reauthorized in 2023 for FY2024-FY2028 (ADUFA V), authorizes the FDA to collect fees for animal drug applications, products, establishments, and sponsors. For FY2026, the full application fee is $708,863, with an establishment fee of $200,000.

These fees supplement congressional funding to enhance predictability and speed in the drug review process, reducing time-to-market for manufacturers.

Veterinary Compounding Oversight: Veterinary compounding is regulated by state Boards of Pharmacy, with federal oversight guidelines from the FDA. Compounding pharmacies must adhere to USP General Chapter <795> for nonsterile preparations and <797> for sterile preparations to reduce contamination or dosing errors.

EU Regulation 2019/6

EU Veterinary Medicinal Products Regulation (2019/6), applicable since January 28, 2022, modernized the European framework. Key differences from the U.S. system include:

- Centralized databases: Union Product Database and pharmacovigilance database for pan-European surveillance

- Antimicrobial surveillance: Mandatory reporting of veterinary antimicrobial consumption data (ESUAvet) to combat resistance

- Import testing: Imported veterinary medicinal products undergo full qualitative and quantitative analysis of active substances within the EU prior to batch release

This divergence from U.S. ADUFA V raises the cost of maintaining legacy, low-margin products in Europe, pushing companies to trim or discontinue lower-margin lines — a trend that reshapes which product categories attract new investment.

For manufacturers operating across both markets, understanding these differences early in development planning avoids costly reformulation or market withdrawal later.

China NMPA Import Requirements

China's Ministry of Agriculture and Rural Affairs (MARA) and National Medical Products Administration (NMPA) strictly regulate imported veterinary drugs. Required documentation includes:

- Approval certification from the country of origin

- Proof of Good Manufacturing Practice (GMP) compliance

- Detailed manufacturing processes and quality standards

- Maximum residue limits for food animal applications

VuRoyal Pharmaceutical completed this process for QS-21 pharmaceutical excipient registration, reaching Public Notice Phase I status in September 2025 — a milestone that typically takes years and requires deep familiarity with NMPA submission requirements.

Antibiotic Stewardship Reshapes Product Mix

Global regulators are restricting medically important antibiotics in food animals. FDA Guidance #213 (2013) facilitated voluntary removal of production uses for medically important antimicrobials. The 2015 Veterinary Feed Directive (VFD) mandated veterinary oversight for these drugs in animal feed.

The financial impact is already visible in industry results:

- –8% decline in Elanco's shared-class antibiotic revenue in 2024

- +4% growth in animal-only antibiotics (primarily ionophores)

This rebalancing is redirecting R&D budgets and procurement demand toward NSAIDs, biologics, and adjuvanted vaccines — categories positioned as the primary prophylactic alternatives going forward.

Supply Chain Integrity and Global Distribution in Veterinary Pharmaceuticals

Why Supply Chain Integrity Matters

Supply chain integrity in veterinary pharmaceuticals directly affects animal health, food safety, and downstream human health. Counterfeit or substandard products jeopardize all three. EU Regulation 2019/6 mandates that wholesale distributors immediately report any suspected falsified veterinary medicinal products, regardless of distribution channel.

Verified sourcing means pharmaceutical buyers can trace products from manufacturer through distributor to end user, with documentation proving authenticity, quality, and regulatory compliance at every step.

Logistical Complexities Specific to Veterinary Pharmaceuticals

Three logistical factors consistently drive procurement decisions for veterinary pharmaceutical buyers:

- Cold chain management: Veterinary biologics and saponin-based adjuvants like Matrix-M require strict 2–8°C storage. Suppliers bear legal responsibility for maintaining manufacturer-defined temperature conditions throughout distribution to prevent degradation.

- Customs and import compliance: Controlled or specialty substances face varying import regulations by country. Distributors must hold current customs declaration certifications and navigate jurisdiction-specific documentation requirements.

- Supply resilience: Recent disruptions exposed single-source vulnerabilities. Elanco paid $130 million to acquire the TriRx Speke facility in 2024 after its contract manufacturer entered administration. Zoetis faced constrained livestock vaccine supply in 2022–2023 until production normalized.

Procurement teams that absorbed these disruptions are now actively prioritizing distributors with verified end-to-end capabilities — not just product availability.

FDA-Registered Distributors as Essential Partners

Under 21 CFR Part 205, the FDA establishes minimum standards for state licensing of wholesale prescription drug distributors. Distributors engaging in interstate commerce must meet specific operational standards, including:

- Secure storage facilities with adequate lighting, ventilation, and temperature controls

- Quarantine procedures for outdated or adulterated drugs

- Transaction records maintained for at least three years to prevent diversion

For pharmaceutical manufacturers and research organizations sourcing veterinary vaccine adjuvants globally, these compliance requirements are a baseline — not a differentiator. What separates capable partners is whether they combine FDA registration with cold chain logistics, customs declaration expertise, and proactive regulatory filing support. VuRoyal Pharmaceutical operates under this framework, providing compliant access to veterinary vaccine adjuvants including QS-21, Vet-Sap, and Ultra through verified supply chains with full regulatory documentation.

Frequently Asked Questions

Are compounded pet meds safe?

Compounded pet medications can be safe when prepared by a licensed, FDA-overseen compounding pharmacy under a valid veterinarian prescription, following USP standards. Quality varies significantly by facility and oversight level, making verification of pharmacy credentials essential.

What is a pharmaceutical vet?

A pharmaceutical vet (veterinary pharmacologist or technical veterinarian) is a veterinary professional specializing in the development, evaluation, and application of pharmaceutical products in animal health. They play key roles in R&D, regulatory submissions, and clinical research for veterinary drugs.

What is driving the growth of the veterinary pharmaceutical market?

Rising pet ownership, food security demands, zoonotic disease pressure, the One Health framework, and increased R&D investment are the primary factors expanding the global veterinary pharmaceutical market — driving demand across companion animal, livestock, and poultry segments alike.

How do vaccine adjuvants contribute to animal health?

Adjuvants boost and prolong the immune response triggered by animal vaccines, enabling stronger protection with lower antigen doses. For large-scale livestock and poultry programs, this dose-sparing capability reduces costs while improving cross-protection against evolving viral strains.

What regulations govern veterinary pharmaceutical distribution in the United States?

The FDA's Center for Veterinary Medicine (CVM), state Board of Pharmacy licensing, and drug business license requirements govern distribution. Distributors must maintain secure facilities, complete transaction records, and adherence to USP standards to operate legally within the U.S. veterinary pharmaceutical supply chain.

How does global supply chain disruption affect veterinary drug availability?

Disruptions to cold chain logistics, international customs delays, and reliance on single-source API manufacturers can limit access to critical veterinary medicines. These vulnerabilities underscore the value of certified, multi-qualified distributors with established global procurement networks and regulatory expertise across multiple jurisdictions.